If you have no credit history or are rebuilding your credit, qualifying for a credit card or loan may be challenging.

You could try a secured credit card, but you typically must have money for the deposit. A credit-builder loan offers consumers a chance to build credit — or rebuild credit — without requiring money upfront.

A credit-builder loan operates the opposite way of how traditional personal loans work. With a traditional loan, you receive the loan funds right away and make payments throughout the specified term.

With a credit builder loan, the loan amount is held in a certificate of deposit or savings account for the duration of the term. You make monthly payments to the lender, and you receive your money (minus interest and fees) after you’ve finished making payments on the loan.

Self is a lender that offers a credit-builder loan to U.S. residents in all 50 states. Here’s what to know.

How a Self credit-builder loan works

If you’re approved for a Self credit-builder loan, the loan amount is deposited in a certificate of deposit with one of Self’s FDIC-insured partner banks. You’ll make monthly payments over the loan term. After all payments are made, you get access to the money minus fees and interest.

Self offers two-year terms for four different monthly payment options. The lowest payment is $25 a month. You can also choose payments of $35, $48 or $150 per month.

Self reports your payments to the three major credit bureaus: Equifax, Experian and TransUnion. Any late payments will hurt the credit you’re trying to build.

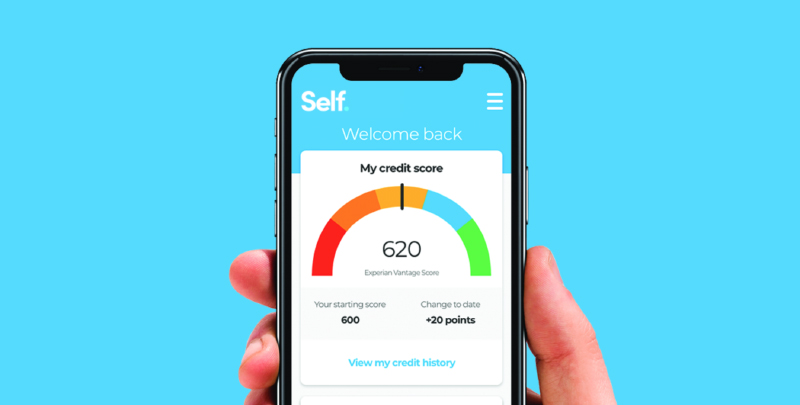

After about six months, your repayment activity should generate a FICO score if you didn’t already have one. Your VantageScore can be generated sooner.

During the repayment period, you have access to free credit monitoring and a VantageScore so you can track your credit score’s progress.

🤓Tips

A credit-builder loan is different from a secured credit card in two important ways. First, you don’t need money upfront to get the loan. With a secured card, you typically have to pay a deposit upfront, and that amount is generally your credit limit. The other major difference is that you cannot access the money from a credit-builder loan until the loan is paid off. With a secured card, you can use up to your credit limit anytime — though doing so will increase your credit utilization and can hurt your credit until the balance is low again.

Pros and cons of a Self credit-builder loan

Pros

No hard credit check.

On-time payments are reported to the three major credit bureaus.

Cons

You don’t receive funds until after you’ve made all the payments.

Missed payments can damage your credit.

How to qualify for a credit-builder loan with Self

The loan application is submitted online. To qualify, you must be at least 18 years old and may be asked to meet the following requirements:

-

Be a permanent U.S. resident.

-

Have a Social Security number.

-

Have either a bank account or debit card; a prepaid card is OK.

Self rates, fees and penalties

The annual percentage rate for a Self credit-builder loan ranges from about 15.51% to 15.92%, depending on what monthly payment option you choose.

Payments 15 days late or more incur a fee of up to 5% of the scheduled monthly payment. Payments that are 30 days or more past the due date will be reported to the credit bureaus, likely damaging your score.

Self secured credit card and other financial products

In addition to the credit-builder loan, Self offers other financial products to help boost your credit or fulfill borrowing needs.

Self secured credit card

Self offers a secured Visa credit card. You can use money you have paid on your Self loan account to secure the credit card.

There’s no hard credit inquiry, and — like the loan — the secured card reports your payments to the three major credit bureaus.

Opening a Self secured credit card in addition to a Self credit-builder loan gives you two types of credit: revolving (the credit card) and installment (the loan). This could help build credit faster because the scoring formulas reward consumers for handling different types of credit responsibly.

Rent and bills reporting

You can opt into having Self report your rent payments to the three credit bureaus for free — or pay a monthly fee for the company to report other bill payments to TransUnion. A record of on-time payments can help build your credit score.

Self Cash

Self offers cash advances to borrowers in 35 states. Eligible individuals can borrow up to $300 and repay the advance on their next payday.

Getting a cash advance doesn’t require a hard credit check, but you also won’t build your credit score. The service is free if you’re fine with waiting up to three business days for the money. For instant delivery, you’ll be charged a fee.

Sample product: $25/mo, 24 mos, 15.92% APR; $35/mo, 24 mos, 15.69% APR; $48/mo, 24 mos, 15.51% APR; $150/mo, 24 mos, 15.82% APR. See self.inc/pricing. Credit Builder Accounts & Certificates of Deposit made/held by Lead Bank, Sunrise Banks, N.A., First Century Bank, N.A., each Member FDIC. Subject to credit approval. The secured Self Visa® Credit Card is issued by Lead Bank, Sunrise Banks, N.A., or First Century Bank, N.A., each Member FDIC. The secured Self Visa® Credit Card can be opened with your active Self Credit Builder Account savings progress to secure your card and set your limit. Qualification is based on other eligibility criteria including income & expense requirements. Criteria subject to change.

Other ways to build your credit

If you have little credit history or a low credit score, here are other options to build your credit.

Make consistent payments on a traditional personal loan

Some online lenders and credit unions offer personal loans to applicants across the credit spectrum. Opting for a secured personal loan or applying with a co-borrower or co-signer could increase your chances of loan approval. On-time payments reported to the credit bureaus can boost your credit score.

If a family member or friend who has a strong credit history adds you as an authorized user, their on-time payments can benefit your credit standing. You don’t even need to get a separate credit card or have to use the card yourself.

Pay down your credit cards or other revolving credit accounts

As you pay down your revolving debt, you’ll lower your credit utilization ratio — which is the amount of revolving credit you’ve used compared to your credit limits. A lower credit utilization ratio can positively affect your credit score.